There are many ways of running your own business. And one of the most popular structures people choose in the UK is the limited company.

Having your own company has many advantages and also some drawbacks. Before you start one, you should know exactly what you let yourself into.

Here at Business4Beginners we have been running our own company for several years now.

Drawing on our experience, we will answer all your questions about starting, owning and running a limited company, so you know what it involves.

Starting A UK Business?

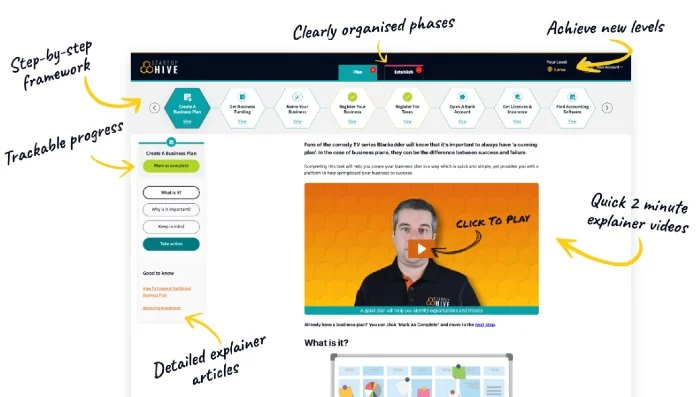

Get rid of the confusion and always know what to do next with Startup Hive, the step-by-step platform created by the Business4Beginners team.

- FREE Step-By-Step Platform

- FREE Bank Account

- FREE Bookkeeping Software

- FREE Email Platform

- FREE Domain Name

- Discounted Company Formation

- Plus Much, Much More!

Join today for 100% FREE access to the entire Plan & Establish phases, taking you from validating your business idea through to setting it up, getting your accounts sorted, and creating a website.

“Excellent guide to build your business”

“The perfect starting point”

“Incredibly simple and intuitive to use”

Startup Hive is your trusted companion as you look to turn all of your business dreams into reality. Join today for free.

—

What is a limited company?

A limited company is a registered company that has shareholders who have an active interest in the company making money.

The shareholders will receive a share of the declared profits of the company depending on the number and type of shares they own. Limited companies can be owned by a single person and shareholder or multiple people.

Limited companies have more legal responsibilities than, for example, sole traders but also offer more options available to improve tax efficiency for their owners.

A limited company is also its own legal entity, which means it can own assets and be sold on. And as the name says, it has limited liability, which can be great benefit.

How do you set up a limited company in the UK?

Setting up as a limited company is still relatively straightforward.

Here are the steps we recommend:

- Decide on a catchy name for your business.

- Choose a company formation agent to register your limited company. They will take all the legal steps necessary to register your company with Companies House.

- Create a company bank account and start following basic bookkeeping practices to keep everything in order (you will find accountancy software makes this job much easier).

- Register for Corporation Tax or hire an accountant who will do this for you.

- Ensure you stay on top of all your annual filing requirements.

Not that scary after all, huh?

While you don’t have to use a company formation agency, it makes things much smoother and easier. And you can be sure that everything is done correctly.

Which Company Formation Package Is Right For You?

Answer 5 multiple choice questions to get a personal recommendation:

What are the pros and cons of a limited company?

Being a limited company has its pros and cons like everything else. And knowing both sides of the coin will help you decide if it’s the right one for your venture.

So let’s start with the benefits:

- Liability – there is only limited liability for owners and directors as the company is its own legal entity

- Lower taxes – running a limited company means that the owner pays less taxes

- Reputation – a limited company is often perceived as more professional and trustworthy

- Better investment chances – a limited company will find it easier to find investors

- Company name protected – nobody will be able to register a company with the same or similar name

These are quite some benefits. But what about the drawbacks?

- Set-up – it’s more complicated to register a limited company and a fee applies too

- More regulations and reporting – a limited company has to adhere to quite a few regulations and reporting reuqiremnts

- Higher running costs – the above lead to higher running costs

- Less privacy – your details will appear on the Companies House public register

If you want to know more, read our article about the pros and cons of a limited company.

Recommended – Top-Rated Online Accountant:

What is the ICO data protection fee?

Once you have registered your business with Companies House, you will receive a letter from the ICO about paying the ICO data protection fee.

When we got this letter, we first thought it was a scam, because we’d never heard about it before. So what is it?

The Information Commissioner’s Office (ICO) is a non-departmental public body that makes sure that companies adhere to data protection laws.

Basically, they make sure that any of your data held by a company, such as email address, home address, name, date of birth, etc., is handled safely and according to current legislation.

As part of the Data Protection Act 2018, which regulates how your data is handled by companies and other official bodies. As part of this act, it became a law that any business that processes personal data has to pay an annual fee, the ICO data protection fee.

The money raised is then used to fund the work of the ICO to ensure our data is protected.

Do you have to pay it?

While there are exemptions, the chances are your business has to pay the fee. The criteria are that you have to pay the fee if you process personal information electronically or use CCTV images for crime prevention.

The first one is the one that will mean most businesses are liable to pay the fee. Even if all you do is collect email addresses from your customers/users, you might have to pay the fee.

If you send out goods, you will hold people’s names, addresses, email addresses, card details, etc., and it’s very likely to have to pay the fee.

The ICO provides an assessment tool which you can use to find out if you need to pay the fee. You have to answer a series of questions about if, how and why you process data. It takes about 10 minutes to complete.

How much do you have to pay?

The amount you have to pay will depend on how big your business is and how much annual turnover you have. There are three tiers:

- Tier 1 – if you have less than 10 staff members OR a maximum annual turnover of under £632,000 – you pay £40 or £35 if you pay by direct debit

- Tier 2 – if you have between 10 and 249 staff members OR a maximum annual turnover doesn’t exceed £36 million – you pay £60 or £55 if you pay by direct debit

- Tier 3 – if you have 250 staff members or more OR an annual turnover over £36 million – you pay £2,900 or £2,895 if you pay by direct debit

Small businesses are likely to fall into tier 1, maybe tier 2, so the costs aren’t huge. But if you don’t pay, you could incur fines between £400 and £4,000.

The ICO will send you a letter every year when the fee is due, or you can set up a direct debit, which also reduces the fee.

Get it taken off your to-do list

If you don’t want to have to worry about this every year, you could outsource it to a company formation agency. Our recommendation would be 1st Formations, who offer an ICO Registration Service.

For a yearly fee of £79.99, they will register you with the ICO and pay the fee on your behalf, so you can just forget about it. All you have to do is answer a questionnaire when you first buy the service, and they will do the rest.

You can buy their service when you form your company with them as part of the formation process. All you have to do is choose the service on the “additional services” page.

You can add the service later if you have already registered your company with them, using their Online Company Manager account.

If you haven’t formed your company with them, you can create your Online Company Manager account with them for free and then buy the ICO registration service through there.

All you have to do is import your company details to set up the free account. Then you can get access to their various services.

How to change the name of a limited company?

There are reasons to change your company name, for example, if it no longer with the business. The good news is that it’s possible to do so. There are two ways to do it: manually with Companies House or using a company formation agency to do it for you.

Here is how you do it manually:

- Decide on a new name

- Choose the method of change – special resolution or permission through means of article of association

- Submit your name change to Companies House – can by done via software, online or post

- Pay the fee – £20 if you use software or online and £30 if you do it by post

- Display your new name – this means on your website, premisses, stationary, etc.

- Inform relevant organisations – bank, insurance, relevant official bodies, etc.

- Communicate new name to customers/clients

If you want to make the process quicker and less work, you can use a company formation agent to do it for you.

Recommended Company Name Change Service:

If you’re looking for an affordable way to change your company name without having to complete lots of complex forms yourself, we recommend using the 1st Formations ‘Change of Company Name’ service.

For a very reasonable fee, they’ll complete and file the NM01 form at Companies House and also provide all related documents such as a resolution, minutes, and certificate of name change.

Click here to visit their site

Get more details on the individual steps in our guide about how to change your company name.

How to extract profit from a limited company?

There are several ways you can get money out of your business, if you wish to do so:

- Wages

- Dividends

- Pension

Each of these methods will incur different taxes, so it’s important that you choose the right one for your situation. On wages you will have to pay income tax.

On dividends you have to pay dividend tax. If you aren’t the only shareholder, you also have to pay out dividend to all the other shareholders according to the number of shares they own. So you wouldn’t get 100% of the money you extract form your business.

Your company can pay into your pension pot for which you won’t have to pay taxes. But you can only get your hands on this money once you have retired.

If you want to know more detailed information, read our guide about how to extract money from your business.

It can sometimes be difficult to figure out what’s the most tax-efficient way to extract money from your company, so it might be worth asking an accountant for advice.

Top-Rated Online Accountants:

| Accounting Software | Cheapest Package | Value For Money | Our Rating | Review | Official Site |

|---|---|---|---|---|---|

| £24.50/mo | Excellent | 9.4 | Read Review | Visit Website |

| £42/mo | Good | 9.3 | Read Review | Visit Website |

| Variable | Good | 9.1 | Read Review | Visit Website |

Do you need a company secretary as a limited company in the UK?

The short answer is no, you don’t. However, a company secretary fulfils an important role. It’s not just a receptionist or personal assistant, as many people think.

In fact, it’s an officer role, which means a company secretary is part of the management team. Their responsibilities can be numerous and will depend on the nature of the business but can include:

- Ensure rules, laws and regulations are adhered to

- File confirmation statements and company returns

- Maintaining statutory books and registers

- Liaise between directors and shareholders, including organising and minute meetings between them

- Managing the office address

- Keep business documents safe

The list goes on and on. So what if you decide not to have a company secretary? Well, in this case it’s up to the director/s or a person authorised by them to take on these responsibilities.

Depending on the size and nature of your business, it might not be necessary for you to have a secretary. But if you need one, you can either hire someone to fulfil the position or outsource it.

Recommended Company Secretary Service:

Prefer to outsource your company secretary so that it’s one less thing to worry about?

Our top-rated company formation agent, 1st Formations, offer a full company secretary service (even if you didn’t use them to form your company).

It includes a named secretary at Companies House, a dedicated account manager, and maintenance of your statutory registers – including your annual confirmation statement.

Click here to visit their site

Can you run a UK limited company from abroad?

Yes, you can. But you will have to adhere to the standard obligations like any other UK limited company. This means you have to:

- Pay Corporation Tax

- Annually submit Confirmation Statements and Company Accounts

- File your company tax return every year

You also have to follow regulations regarding accounting and company records, which have to be kept safe and up-to-date.

One thing you might struggle with is getting a UK bank account, as most banks require you to be a UK resident. However, the big chains like HSBC, Barclay’s and Lloyds Bank might offer UK bank accounts for non-residents under certain circumstances.

One thing you need to keep in mind is that you might be liable to paying income tax on any earning you make while in the UK. This can be tricky to figure out, so we would recommend to have an accountant to make sure you pay your due but not more.

Setting up a UK company as a non-resident works the same way as for a UK resident. However, you will need a UK address to do so, and it can’t be a PO box. You can buy a business address from company formation agencies, so you don’t have to worry about living or owning a property in the UK.

A company formation agency can also help you to set up your UK company for you, taking out a lot of the hassle and stress.

Forming a UK company as a non-resident?

You’ll need to use a UK company formation that is experienced in providing company formations for non-residents.

We recommend 1st Formations as they offer a ‘Non-Residents Package’ that includes everything you need including UK business banking, 12-month cancellation protection, London registered addresses with International mail forwarding.

Click here to view the Non-Residents Package

Want to know more about this topic? Read our article about running a UK company from abroad.

What expenses can I deduct as a limited company?

One of the perks of owning a limited company is that you can use expenses to reduce your tax bill. But what are they?

Generally speaking, any money you spend as part of running your business or that are “wholly, exclusively, and necessary” for business purposes can be expensed. Here are some examples of things that are classed as allowable expenses for a limited company:

- Travel costs – as long as they are for business purposes

- Accountancy fees – this includes fees charged by an accountant for for accountancy software

- Bank charges

- Insurance that is necessary for running your business

- Relevant equipment – like computers, printers, monitors, desks, machinery, tools, etc.

- Legal fees – if your company needs legal advice

- Software/web hosting – if you have a website and need to buy special software or pay for web hosting

There are many more allowable expenses, you can find out more in our article about 25 allowable expenses for a limited company.

What’s the difference between a sole trader and a limited company?

Most people who want to start a business decide between two structures: a sole trader or a limited company. So understanding the difference between both is important.

The main difference is in the legal status. As a sole trader you are the business. In contrast, a limited company is its own legal entity. From this main difference spring other differences:

- A sole trader is fully liable for their business, whereas a company owner only has limited liability

- You pay different taxes: income tax as sole trader and corporation tax as limited company

- Regulations: limited companies have to adhere to more regulations and reporting requirements than sole traders

- You can sell a limited company but not a sole trader business

- Only one person can own a sole proprietorship, but several people can own a limited company

- Solder traders tend to have lower running costs than limited companies

- Setting up a sole trader is quick, easy and free, whereas the process to set up a limited company is more complex and comes with a fee

Want to know more about this topic? Read our article about the difference between sole traders and limited companies.

Can I switch from a sole trader to a limited company?

The simple answer is yes. And it’s very simple to do as it’s only a few steps you have to take.

First you have to register your business as a limited company with Companies House. You can do this yourself directly or use a company formation agency, as we have described earlier.

Then you have to let HMRC know that your business has changed structure. You have to submit a final self-assessment tax return to ensure that you have paid what you are due.

You will need to transfer any assets to the new company, for example, equipment. And as a limited company you will need a business bank account.

Another important step is to register for Corporation Tax, which has to be done within three months of the date of incorporation.

You can find more information about the steps to take in our guide about switching from sole trader to limited company.

When to switch from sole trader to limited company?

As we have said, many people start their business as a sole trader and than switch to a limited company as it grows. The big question is at what point to change structure.

While there isn’t a hard and fast rule, like after 2 years, there are questions you can ask yourself to determine if it’s time time make the switch. If you answer yes to one or more of these, than your business is at a point where the change is advisable:

- Are your profits high? – earning more than £15,500 per year would be considered as high enough

- Do you want to sell you business?

- Are you looking for more investment?

- Do you want to attract high-profile clients?

For more detailed information, read our guide about when to switch from sole trader to limited company.

Can I switch from a limited company to sole trader?

Yes, however, it’s a more complex process than the other way round, due to the first step you have to take:

- Disslove/wind up your limited company

- Inform HMRC that of the change of structure

- Register for self-assessment tax returns, if not already registered

- Inform all stakeholders of your business

- Update public areas, such as website and stationary, to reflect the change

Because you have to close down your company, it could take longer. It’s worth taking this into account and plan in the extra time.

FREE Download:

The Business Success Planner

Set clear goals for your business

Plan and manage your time more effectively

Brainstorm ideas and log inspirations

Stay motivated and encouraged

How do you close down a limited company?

Winding up your business can be a sad affair, but sometimes it’s the only thing to be done. Or maybe you are retiring, which is a more joyous reason. Either way, there is a process to follow, but first you have to decide which method to use.

If your business is insolvent, which means it can’t pay its bills anymore, you have to put it into administration or opt for Creditor’s Voluntary Liquidation (CVL).

The government website will guide you through these options if that’s the routes you have to take.

If your company is solvent, you have two options: Member’s Voluntary Liquidation (MVL) or striking off your company from the register. Using a MVL means you need to appoint a liquidator who will wind up the company once the directors have signed the declaration of solvency.

MVL will take longer, but you will avoid having to pay income tax on your profits as well as capital gains tax. The process can take up to 12 months.

Voluntarily striking off your company from the register is much quicker. Here are the two steps you have to take.

- Stop trading – this has to happen three months before the actual dissolution, which gives you time to complete all necessary admin tasks, like paying outstanding debts and closing your bank account

- Submit the DS01 form to Companies house – you will have to pay a fee and the company will be struck off the register after three months if nobody objects

Which of these options you choose will depend on the individual circumstances of your business and your own preferences.

Find out more in our article about how to dissolve a limited company.

Looking for more tips on setting up your business? Check out our ideas and tips here.

Top-Rated Accounting Software:

| Accounting Software | Cheapest Package | Ease Of Use | Our Rating | Review | Official Site |

|---|---|---|---|---|---|

| £33/mo | Excellent | 9.4 | Read Review | Visit Website |

| FREE | Outstanding | 9.3 | Read Review | Visit Website |

| £10/mo | Excellent | 9.3 | Read Review | Visit Website |